CPA Evolution - 2024 CPA Exam changes.

The new CPA Exam launched in January 2024. Make sure understand the new exam format and transition policies with our free resources.

See how the new Becker CPA Exam Review gets you Exam Day ReadySM for CPA Evolution! This on-demand webinar showcases our new, engaging content, product upgrades, and live, virtual learning opportunities.

See how the new Becker CPA Exam Review gets you Exam Day ReadySM for CPA Evolution! This on-demand webinar showcases our new, engaging content, product upgrades, and live, virtual learning opportunities.

See how the new Becker CPA Exam Review gets you Exam Day ReadySM for CPA Evolution! This on-demand webinar showcases our new, engaging content, product upgrades, and live, virtual learning opportunities.

Not sure which Discipline Section is right for you? Becker has resources to help! Start by taking our 4-question quiz to guide you in the right direction.

Not sure which Discipline Section is right for you? Becker has resources to help! Start by taking our 4-question quiz to guide you in the right direction.

Not sure which Discipline Section is right for you? Becker has resources to help! Start by taking our 4-question quiz to guide you in the right direction.

Candidates preparing for the new CPA Exam

Becker has seen its fair share of changes to the CPA Exam over our 60+years. And we've met each one with the resources, instruction and guidance to help over 1 million candidates get their CPA license. Now, we're greeting CPA Evolution with a more engaging, personalized experience to get you Exam Day ReadySM.

All Becker students will receive access to CPA Evolution content on October 3, 2023. Check out the exciting CPA Exam Review enhancements.

July 2023

All Becker students will receive access to CPA Evolution content on October 3, 2023. Check out the exciting CPA Exam Review enhancements.

July 2023

All Becker students will receive access to CPA Evolution content on October 3, 2023. Check out the exciting CPA Exam Review enhancements.

July 2023

Feel confident in choosing Becker as your CPA Exam review partner. Enroll in a 14-day trial and get access to the same platform you will use during your review journey with Becker.

Feel confident in choosing Becker as your CPA Exam review partner. Enroll in a 14-day trial and get access to the same platform you will use during your review journey with Becker.

Feel confident in choosing Becker as your CPA Exam review partner. Enroll in a 14-day trial and get access to the same platform you will use during your review journey with Becker.

Check out Becker's recommended order to take the new CPA Exam in 2024 based on your discipline.

Check out Becker's recommended order to take the new CPA Exam in 2024 based on your discipline.

Check out Becker's recommended order to take the new CPA Exam in 2024 based on your discipline.

Not sure which Discipline is right for your career goals? Take our quiz and find out!

October 2023

Not sure which Discipline is right for your career goals? Take our quiz and find out!

October 2023

Not sure which Discipline is right for your career goals? Take our quiz and find out!

October 2023

This asset includes important dates as the CPA Exam transitions including: exam application deadlines, last day of testing in 2023, first day of testing in 2024 and tentative testing schedule/score release windows in 2024.

January 2023

This asset includes important dates as the CPA Exam transitions including: exam application deadlines, last day of testing in 2023, first day of testing in 2024 and tentative testing schedule/score release windows in 2024.

January 2023

This asset includes important dates as the CPA Exam transitions including: exam application deadlines, last day of testing in 2023, first day of testing in 2024 and tentative testing schedule/score release windows in 2024.

January 2023

CPA Evolution for Educators and Firm/Corporation Administrators

Our team of instructors, CPAs and accounting curriculum junkies, know what it takes to help students succeed, and we remain committed to your students, staff and recruits become CPAs. Lean on Becker to learn about the new CPA Exam and all things CPA Evolution.

Check out the exciting CPA Exam Review enhancements for CPA Evolution launching on October 3, 2023.

July 2023

Check out the exciting CPA Exam Review enhancements for CPA Evolution launching on October 3, 2023.

July 2023

Check out the exciting CPA Exam Review enhancements for CPA Evolution launching on October 3, 2023.

July 2023

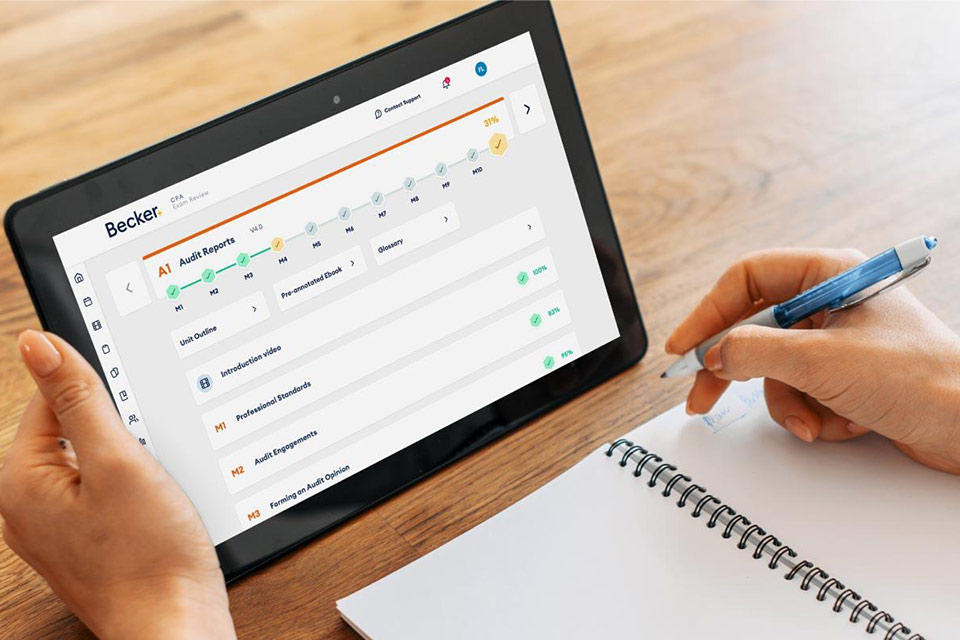

Get an overview of Becker's new CPA review course in an in-depth webinar that's available on demand.

Get an overview of Becker's new CPA review course in an in-depth webinar that's available on demand.

Get an overview of Becker's new CPA review course in an in-depth webinar that's available on demand.

Becker’s extensive library of continuing education helps educators prepare themselves and their students for what’s next.

July 2022

Becker’s extensive library of continuing education helps educators prepare themselves and their students for what’s next.

July 2022

Becker’s extensive library of continuing education helps educators prepare themselves and their students for what’s next.

July 2022

Don’t sweat. Connect with a Becker expert to get your Evolution questions answered.

Don’t sweat. Connect with a Becker expert to get your Evolution questions answered.

Don’t sweat. Connect with a Becker expert to get your Evolution questions answered.

CPA Exam Evolution FAQ

Accounting has evolved over time. CPA Evolution is a joint effort between the National Association of State Boards of Accountancy (NASBA) and the American Institute of Certified Public Accountants (AICPA) that aims to evolve the profession’s licensure model to reflect the technological and data analytics skills and knowledge CPAs increasingly need in today’s marketplace. In short, CPA Evolution addresses those changes with structural and content changes to the CPA Exam effective January 1, 2024.

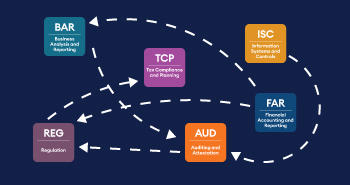

The CPA Exam in 2024 is moving to a Core-Plus-Discipline Model which requires candidates to be skilled in a core base of accounting, auditing, and tax as well as one discipline section. For the discipline section, candidates choose between Information Systems and Controls (ISC), Business Analysis and Reporting (BAR), or Tax Compliance and Planning (TCP). For a detailed explanation of more exam changes for CPA Evolution watch this video.

The new CPA Exam will include three Core Exams. CPA candidates must pass all three:

-

Audit and Attestation (AUD)

-

Financial Accounting and Reporting (FAR)

-

Tax and Regulation (REG)

The CPA Exam will also include three Discipline Exams. CPA candidates must pass just one of the three:

-

Business Analysis and Reporting (BAR)

-

Information and System Controls (ISC)

-

Tax Compliance and Planning (TCP)

Students can sit for the exams in any order, they can even take the discipline exam before the core exams. Once a student passes their first section of the exam, they still have 18 months to pass the remaining three exams.

Students that pass BEC on the current CPA Exam and have credit still on January 1, 2024 will not be required to take a Discipline section. As such, our recommendation is to finish BEC prior to December 15, 2023 (the last day of testing for all sections in the calendar year).

NASBA has released a Transition Policy which provides guidance for students who take some exams prior to CPA Evolution and some exams after the launch of CPA Evolution.

The AICPA and NASBA have also recommended that each jurisdiction adopt the following CPA Exam Credit Extension policy: "Any candidate with Uniform CPA Examination credit(s) on January 1, 2024, will have such credit(s) extended to June 30, 2025." This means that any candidate who has passed at least one section of the CPA Exam and still has credit for that exam on January 1, 2024 will have until June 30, 2025 to pass all remaining sections of the CPA Exam without losing credit for any section passed. Many, but not all jurisdictions have already adopted this Credit Extension policy. To check your jurisdiction status please visit NASBA's website.

If you have additional questions about the new CPA Exam or the NASBA Transition Policy, please contact us at questions@becker.com.

The CPA Evolution initiative is reengineering the CPA licensure module to acknowledge the shift in the skills and competencies needed in the current and future practice of accounting. The new CPA exam will focus on topics that are more relevant in today’s environment which is not necessarily easier or harder but different. If you focus your studies and prepare for the new exam, Becker will be there to support you along your journey.

The CPA Exam is changing to address the need for newly licensed CPAs (nlCPAs) to be more prepared to perform accounting tasks and services that involve the use of technology and data analytics. By preparing nlCPAs in basic and advanced accounting practices, as well as in technology and analytics, nlCPAs will be positioned to be successful throughout their careers in the accounting profession.

The CPA Exam changes are slated to be updated beginning January 1, 2024. NASBA announced a transition timeline for test takers, a test administration schedule, and a score release timeline for CPA Evolution.

Transition Timeline

- August 4, 2023 - Deadline for first-time international candidates for any other exam section to apply with NIES to complete the international evaluation report (required to apply for an NTS)

- October 1, 2023 - Deadline for first-time candidates for BEC to apply for a BEC Exam NTS*

- November 12, 2023 - Deadline for approved re-exam candidates to apply for a BEC Exam NTS*

- November 15, 2023 - NASBA will stop processing BEC exam applications*

- November 22, 2023 - NASBA will start processing applications for the new discipline sections (BAR, ISC, and TCP)

- December 15, 2023 - Last day of testing in 2023 for ALL sections (AUD, BEC, FAR, and REG)

- January 10, 2024 - First day of testing for all CPA Evolution sections.

For more information on transition, test administration schedule and score release timeline, check out this blog.

*These dates apply to the 35 CPA Examination Services (CPAES) jurisdictions. Students in other jurisdictions should check with their individual Board of Accountancy for any BEC application deadlines. Source.

Becker CPA Course Review materials will update on October 3, 2023. We aren't just updating content but rolling out a new and improved Becker CPA Exam Review experience using student feedback.

Becker students will have full access to both the current (2023) exam materials as well as the new (2024) Evolution exam content, both of which will match their respective AICPA blueprints. Students will easily be able to select the version of content they need based on when they plan to test.

So whether you are a current Becker student or plan to be one soon, rest assured that you will have everything you need to pass the CPA Exam now and in 2024 at no extra cost. AND this update and transition will happen seamlessly. We are committed as always to helping you pass the CPA Exam like we have for over 60 years! See how Becker's CPA Exam Review is getting enhanced.

If your Becker course includes printed textbooks, please be aware of the following dates:

- October 2, 2023 - the last day for redemption of textbooks with content designed under the current exam structure (AUD, FAR, REG and BEC)

- October 3, 2023 - textbooks redeemed this day forward will automatically be fulfilled using the new CPA Evolution content structure including updated textbooks for AUD, FAR, and REG, as well as the new textbooks for BAR, ISC, and TCP.

Read Becker's full textbook transition policy here.

Because the changes of CPA Evolution may disrupt your study, Becker will discount replacement printed textbook orders beginning October 3, 2023, through February 3, 2024, for Becker students. During that time, replacement printed textbooks will be discounted from $125 (normal price) to $50 (which includes standard shipping) for any student wishing to order replacement printed textbooks for the new CPA Evolution content.

- For example, if you already have the 2023 FAR printed textbook and plan to take the FAR exam in 2024, you should consider ordering a replacement printed textbook for FAR on or after October 3, 2023 so you can study the updated textbook that is aligned with CPA Evolution.

Individuals who wish to redeem current exam structure printed textbooks (AUD, BEC, FAR, and REG) after October 3, 2023, are urged to contact Becker Customer Service at (877) 272-3926 in the US, or (630) 472-2213 Internationally. Redemption of these textbooks is subject to availability and possible delayed delivery.

Digital textbooks for the new CPA Evolution content will be available in the course beginning October 3, 2023 when Becker's new CPA Exam Review launches addressing the AICPA's revised Core + Discipline format. Students will continue to have access to digital textbooks for the current exam content through December 15, 2023 (the last day of testing in 2023).

In advance of the update to the AICPA's CPA Evolution, Becker is planning to transition away from physical printed flashcards.

- November 15, 2023 - is the last day to order physical printed flashcards, which cover Current Content, testable through December 15, 2023. This date is subject to availability, as supplies last.

- Until December 15, 2023, digital flashcards covering Current Content will continue to be available within the course.

- October 3, 2023 - As previously announced, Becker will release an updated course covering New Content. Beginning on this date, digital flashcards covering new content will be available to all students within their course.

- Select product packages that previously included printed flashcards, will now include Print-able flashcards.

Students with questions are asked to contact Becker Customer Service at (877) 272-3926 in the US or (630) 472-2213 internationally.

Notes:

- Current Content: Reflects the AICPA's existing Exam structure (FAR, AUD, BEC, REG), testable through December 15, 2023.

- New Content: Reflects the AICPA's new CPA Evolution Core (FAR, AUD, REG) + Discipline (BAR, ISC, TCP) model testable beginning January 10, 2024.

Final Review Transition Notice

With the upcoming changes of CPA Evolution in 2024, Becker is upgrading our products and content to match the new exam blueprint. These upgrades will occur on October 3, 2023, except for Final Review which will be updated in 2024. Students can access the current version of Final Review covering content testable until December 15, 2023. Please note that the current version of Final Review will not match the new exam blueprint on October 3, 2023.

A new Final Review, designed for CPA Evolution, will roll out in stages:

- Final Review for CPA Evolution Core Exam sections will be released by January 10, 2024.

- Final Review for CPA Evolution Discipline sections will be released by April 2, 2024.

Final Review Printed Textbook Transition

The 2024 versions of Becker's Final Review will no longer include printed textbooks and instead will feature fully digital materials.

- Printed Final Review textbooks for current 2023 exam content can be redeemed through November 15, 2023 (pending inventory availability).

- Students will continue to have access to digital Final Review textbooks for the current 2023 exam content through December 15, 2023.

Students with questions are asked to contact Becker Customer Service at (877) 272-3926 in the US or (630) 472-2213 internationally.

Discipline Section Selection Policy

As part of CPA Evolution, the AICPA will require CPA Exam candidates to pass all three (3) Core Exam sections (FAR, AUD and REG), and one (1) of the three Discipline Exam sections (BAR, ISC or TCP).

More information on the CPA Exam structure can be found .

Students who purchase on or after October 3, 2023:

All Becker CPA Exam Review packages will include access to content covering all three (3) CPA Exam Core sections. Packages will also include access to content for either one (1) or all three (3) Discipline sections.

For packages that include access to one (1) Discipline section, students will have access to a thirty (30) day trial of all three Discipline sections. This 30-day trial period does not begin at time of purchase, rather students can initiate this trial at any point in their exam preparation from the Manage Sections page at http://cpa.becker.com.

Students will be required to select one (1) Discipline section to continue studying by the end of the thirty (30) day trial.

If a student finalizes their Discipline selection and then wishes to change to another Discipline section, they can only do so by purchasing access to the additional Discipline. An additional Discipline section can be purchased by students at a discounted rate by calling the Becker Inside Sales team at (877) 272-3926 (option 1) in the US or (630) 472-2213 (option 1) Internationally.

For more information on how to choose the right discipline for you, please visit our discipline selection page.

Students who purchase before October 3, 2023:

Beginning October 3, 2023, legacy students who purchase before that date will have access to content covering all three (3) CPA Exam Core sections, as well as access to content for either one (1) or all three (3) Discipline sections depending on which package was purchased.

- For packages that include access to one (1) Discipline section, students will have access to a thirty (30) day trial of all three Discipline sections.

- Students can initiate this trial at any point in their exam preparation from the Manage Sections page at http://cpa.becker.com.

- Students will be required to select one (1) Discipline section to continue studying by the end of the thirty (30) day trial.

- If a student finalizes their Discipline selection and then wishes to change to another Discipline section, they can only do so by purchasing access to the additional Discipline. An additional Discipline section can be purchased by students at a discounted rate by calling the Becker Inside Sales team at (877) 272-3926 (option 1) in the US or (630) 472-2213 (option 1) Internationally.

For more information on how to choose the right discipline for you, please visit our discipline selection page.

Students with questions are asked to contact Becker Customer Service at (877) 272-3926 in the US or (630) 472-2213 Internationally.

Industry resources

- Evolving CPA (evolutionofcpa.org)

- National Association of State Boards of Accountancy

- Association of International Certified Professional Accountants

CPA Evolution in the news

Industry resources

- Evolving CPA (evolutionofcpa.org)

- National Association of State Boards of Accountancy

- Association of International Certified Professional Accountants

CPA Evolution in the news

Industry resources

- Evolving CPA (evolutionofcpa.org)

- National Association of State Boards of Accountancy

- Association of International Certified Professional Accountants

CPA Evolution in the news